Thomas Young

Thomas Young

How to Maximize Your Retirement Savings with a Self-Directed Solo 401(k)

If you’re self-employed, you understand both the freedom and responsibility that come with running your own business. You may also be eligible to...

Working for yourself has some incredible benefits — freedom from early-morning alarms, rigid work schedules, boring daily routines and stifling corporate culture. For many people, self-employment is the ultimate expression of independence, self-worth and personal freedom.

However, working as a self-employed contractor, or padding out your monthly income through side hustles such as driving for Uber or Lyft, has some inherent drawbacks that can be burdensome to overcome. Forgoing a routine paycheck and employer-paid health benefits are but minor obstacles — the primary problem of self-employment for most independent contractors is meeting their hefty tax obligations.

There is a solution: the Self-Directed Solo 401(k)

The freelance and gig-based workforce is booming. A recent study by the Freelancers Union and Upwork reports that 57.3 million Americans performed freelance work in 2017, and nearly 50 percent of all working Millennials are freelancing.

Freelancers, self-employed independent contractors and people who supplement their income using gig-based platforms such as Uber, TaskRabbit, HelloTech and SpareHire can make a good living while enjoying unparalleled personal freedom. Tax time can be scary, though.

Independent contractors who receive a 1099 from the Internal Revenue Service must pay income tax, social security and MediCare taxes on that income. As a rule of thumb, independent contractors pay about 30 percent, give or take, in taxes on their wages. It’s imperative that independent contractors have a savings plan in place so they can meet their tax burden.

Creating a Self-Directed Solo 401(k) through Rocket Dollar helps freelancers and giggers lower their tax bills, as well as creates nest eggs to fund their retirements. Here’s why: Contributions made to a Self-Directed Solo 401(k) are deducted from gross annual income and are not subject to federal income taxes.

In other words, every dollar in is a dollar you don’t pay taxes on. For example, if you earned $50,000 as a freelancer and put $10,000 into a Rocket Dollar Self-Directed Solo 401(k), you are only liable for taxes on $40,000, which can save you hundreds or even thousands of dollars in tax liability. Plus, you’ve invested money into your retirement.

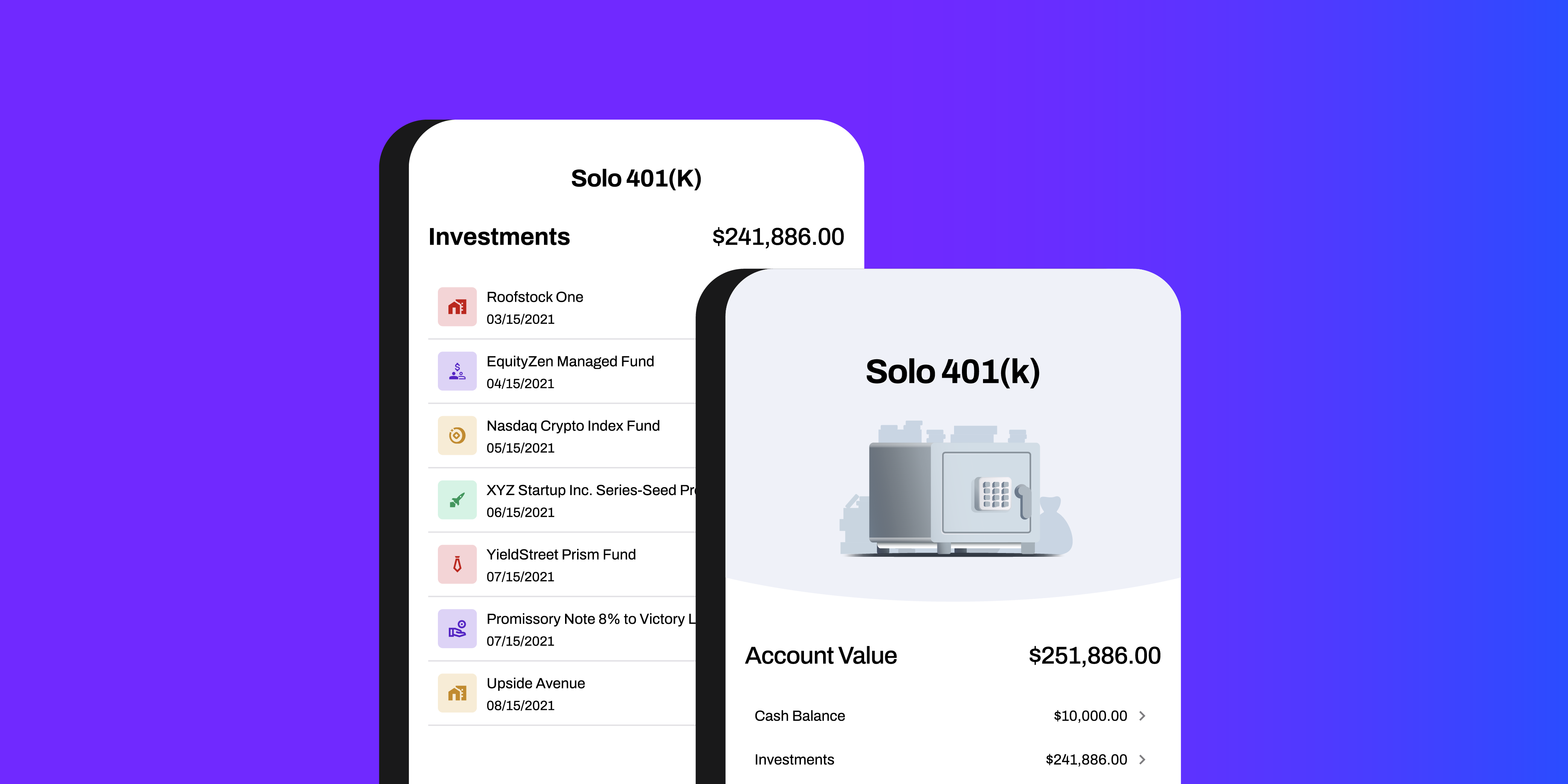

Rocket Dollar provides all the education and paperwork you’ll need to create a Self-Directed Solo 401(k). You also can easily open a savings account or straight brokerage account through Rocket Dollar and set your risk profile accordingly. Freelancers and independent contractors should be aware that there are contribution limits established by the Internal Revenue Service for Self-Directed Solo 401(k)s.

Or, you can explore the full potential of your Self-Directed Solo 401(k) and strategically grow your money through alternative investments.

Wall Street has a long and well-documented history of volatility. Although investors are riding high in today’s bull market with the Dow Jones Industrial Average topping 25,000, it’s important to remember what happened during the last recession. On September 29, 2008, the Dow fell almost 778 points, the largest point drop in history. To quantify, the public markets lost about $1.2 trillion in value in just one day. The DJIA closed the day at 10,365, and by March 5, 2009 it tumbled to 6,594.

Investors still enjoy the financial strength that comes with a strong portfolio of stocks, bonds and mutual funds. However, savvy 21st century investors are creating more diversified portfolios to hedge against the precipitous declines that rocked the world during the last recession.

Freelancers and independent contracts who establish Self-Directed Solo 401(k)s with Rocket Dollar have the flexibility to invest in traditional asset classes and also seek alternative investments such a cryptocurrencies or peer-to-peer loans. Or, say you have a friend that flips houses or builds spec homes. You can be his or her investor through your Rocket Dollar account. Other alternative investment opportunities include early-stage businesses, crowdfunding business deals, tech startups and angel investing.

You have direct control over these investments, which brings a higher degree of comfort since you know exactly where you money is going. Establishing a Self-Directed Solo 401(k) through Rocket Dollar gives you the ability to invest outside of the Wall Street roller coaster. Its 21st century diversification, and it’s a much better hedge against a potential recession.

You can reduce your taxes and decrease the amount of money you have to pay to the government. At the same time, you put yourself in a position to make investments that can produce greater returns. You get a tax abatement on your income and a tax abatement on your gains, and you have the power to create those returns and not leave it in hands of someone else.

If you’re self-employed, you understand both the freedom and responsibility that come with running your own business. You may also be eligible to...

In today’s investing landscape, many individuals are asking the question: What are the benefits of investing in alternative assets? As traditional...

Alternative asset investment is no longer reserved for hedge funds and institutional players. Thanks to platforms like Rocket Dollar, everyday...

Tax time can fill anyone with trepidation, but the apprehension of looming tax liability can be especially worrisome for independent contractors,...

If you’re self-employed, you understand both the freedom and responsibility that come with running your own business. You may also be eligible to...

For entrepreneurs, freelancers, and self-employed individuals, it can sometimes feel like your retirement account options are limited. Traditional...